We can help either way. Click on the Articles button on the menu bar above to go to publically available videos and articles,

© 2025 Your Legal Leg Up, All rights reserved

There is unfortunately little you can do in talking to student loan collectors. Most of the time, the debt collectors themselves really have little right to negotiate with you. The law behind student loans is that they are not dischargeable in bankruptcy absent “extraordinary” circumstances and “undue hardship,” and the cases discussing the issue have been extremely unpromising, to say the very least, about what circumstances must be in order for them to be “extraordinary.” “Undue hardship” has been interpreted to mean “no likelihood of ever being able to pay the debt,” an almost unprovable burden. On the bright side, there are increasing numbers of organizations and programs out there to help, and the lending institutions have not seemed eager to sue anybody.

One of the programs that might help you deal with student loans (not a negotiation) is an “income-based” payment (IBR) program. The plans call for a payment “cap” of a certain percentage of discretionary income and provide for loan “forgiveness” after a certain period of time. The program seems, at first sight, to be very reasonable, with a limit on payments and amount of time that will be required. They are for federal loans.

Another sort of help is available if you are doing some sorts of public or nonprofit service as your job, you may be able to get help from the federal government. Click here for the link that will take you to the government site discussing that help. This program is designed for only certain kinds of loans. Here’s what the government says about it:

Only loans you received under the William D. Ford Federal Direct Loan (Direct Loan) Program are eligible for PSLF. Loans you received under the Federal Family Education Loan (FFEL) Program, the Federal Perkins Loan (Perkins Loan) Program, or any other student loan program are not eligible for PSLF.

If you have FFEL Program or Perkins Loan Program loans, you may consolidate them into a Direct Consolidation Loan to take advantage of PSLF. However, only payments you make on the new Direct Consolidation Loan will count toward the required 120 qualifying payments for PSLF. Payments made on your FFEL Program or Perkins Loan Program loans before you consolidated them, even if they were made under a qualifying repayment plan, do not count as qualifying PSLF payments.

There are serious limits to the kind of help this offers, but for some people this will be a way out of difficulty. Click here for more information.

Another, similar program, the “Pay as You Earn” program, is, like the IBR program above, based on a type of financial hardship. The program provides for payment caps and loan forgiveness if your payments would be too much for you to be able to afford under the standards established by the program. You can find out about that here: Pay as You Earn.

For more help on student loans, you should check out the Project on Student Debt. If you aren’t sure what kind of loans you have, check out the National Student Loan Database System for Students and select “Financial Aid Review” for a list of all the federal loans to you. Click each individual loan to see who the servicer is for that loan (this is the company that collects payments from you). Remember that system shows only your federal student loans, however, and not your private or state student loans. Contact your school to see whether you have non-federal loans if you are in doubt about that, as they keep a record of them.

For more information on student loans and repayment, check out consumer finance. If you are active-duty military, there may be benefits helpful to you under the Service Members Civil Relief Act. If you’re not in the military and have private loans, you have fewer options, but take a look at: Paying for College. For an article on reducing student debt without paying for it or click here for a free ebook on ways to get rid of student loans without paying for them

One of the options we found interesting was the public service type loan forgiveness program that also helps with state or private loans

Unfortunately, there’s really very little or even no negotiating with debt collectors on student loans, as we said above. There seem to be no market pressures on them to settle at all – they aren’t worried about the debt expiring, the companies that issue the debt are large and government-subsidized, and “educational loans” are one of the last great sacred cows in our country.

The positive side of dealing with student loans, however, is that while the collectors will call and bug you, somebody in the collection department usually does seem to take notice of the actual financial reality you are facing. If you tell them that you do not have the money to pay, they will often – usually even, it seems, refuse to agree to partial payments – but then they usually don’t take any type of collection action, either, and they only very rarely sue anybody. The downside here is still significant, however, as the information might very well end up on your credit report and cost you that way. And eventually the lender might get around to suing you after all if they find out you have property, so they may create problems if you own your home.

How hard is it to defend yourself from the debt collectors? The difficulty is mostly psychological. It can be scary at first, but if you do the things that need to be done one at a time, it isn’t that hard. And you have a great chance to win.

It isn’t that difficult to defend yourself from the debt collectors. It just requires that you do some things that take you out of your comfort zone – more a question of attitude than anything else. The work is really just a series of steps. Each one involves a manageable amount of learning and doing, and the more you do the better you get at doing it.

It will take some work, of course, and sometimes it may be frustrating, but you can do it, and the rewards can really be great. You will be able to do something it would cost you hundreds or thousands of dollars to get someone else to do for you, and you’ll know they’ll never be able to push you around again.

Our mission is to protect people from the debt collection process. If you are being sued by debt collectors, or if you are being harassed for money, you need to take action to defend what’s yours. For much more information on defending yourself, go to Fast Track to Debt Defense.

If you’re a pro se debt defendant or thinking about doing that, welcome to our site.

If you are already representing yourself in a debt lawsuit – or if you think you might want to – you will find the help you need here. In addition, you will find hope and encouragement to take the steps you need to take to protect your rights.

It may seem like the deck is stacked against you, but you have an excellent chance to win and get out of this in good shape. That’s because of the way the system is designed – the debt collectors run a factory, and that leaves you plenty of opportunities to protect yourself. We tell you why, below.

As you look at this site, you will probably notice that we spend a lot of time trying to persuade people they can defend themselves from debt collection law suits. The main challenge in self-representation is often just being able to make yourself take the next step. It can seem hopeless or hopelessly complicated, so taking any action can require a leap of faith. We want to help you with that, because most people who represent themselves with our help actually do win.

Of course it takes more than encouragement. You have to do some right things, but debt law is not all that difficult to understand. With some basic help you will have an advantage in defending your rights.

With a little courage, and help from this site, you will be able to defend yourself competently. Enough to make them take notice. Enough to cost them money. And, often, more than enough to win or make them go away and leave you alone.

You’ll learn something pretty great about yourself on the way. You have power, and you can defend yourself from people who are trying to take things away from you.

Good can come of bad

These are the plain facts as far as we know them.

No one really knows exactly how many debt lawsuits are filed each year. The numbers are not kept in any central location. Our guess is that the number is at least a million per year.

No one really knows exactly how many of these suits are won by default, or even how many actually get served on the defendants. And of those that do get served and defended, no one actually knows how many are won by defendants. The number that lawyers who defend many of these cases usually use is that between 80 and 90 percent of the cases that get served are won by the debt collectors by default. We would estimate from our own experience and observation that around 90-95 percent of the cases are disposed of without a defense –i.e., that defendants either default or settle on the day of court by agreeing to pay everything claimed in the lawsuit.

If that seems like a big number, it is. In most kinds of law the default and give-up rate is much, much smaller. But this will work out to your advantage if you will actually fight.

Of the lawsuits that are defended, no one really knows how many are won by the defendants or the debt collectors, or what the terms of any settlements actually are (nationally). From our experience and research, we would estimate that at least 80 percent of cases that are defended with any significant effort and knowledge are “won” by defendants. We consider a settlement for a small fraction of the amount sought a victory for the defendant.

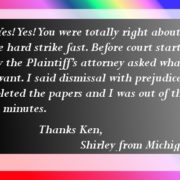

Of the lawsuits defended pro se by users of YourLegalLegUp, most result in dismissal without payment, and almost all the rest result in settlement for what you might call a “token amount.” It would appear that members of Your Legal Leg Up do much better than those represented by lawyers who do not specialize in debt defense.

A Caution: Not every customer has told me the outcome of his or her case.

You are not alone

The reason it works this way is not magic. It’s simply that debt collectors generally do not have the materials they need to win their lawsuit when they file suit against you.

Because they win most of their cases without a fight, it isn’t worth the expense of getting lawsuit materials before they need them, and the people who sold them the debt do not want to be troubled by it any more. The original creditors actually resist giving the debt collectors the documents they would need to beat you and sometimes destroy the records or make the debt collector promise not to seek them. In other words, the debt industry works by getting people to give up. If you fight – and keep fighting for a while – they may well lose interest or simply lack what it takes to beat you in court.

Lawyers who specialize in debt defense know that debt collectors do not have the materials they need to win and have to spend money to get them. These lawyers know how to expose the weaknesses of the debt collectors’ cases and force the debt collectors to spend money trying to get the evidence they need and defending against counterclaims and motions. The debt collectors know these lawyers and what they can do and choose not to fight most of the time.

Lawyers who do not specialize in debt defense often suggest you settle the case right away. They do not know what debt collectors have or need and find it expensive to try to defend the cases. They often tell their clients that it will cost more to defend than is in dispute in the case. And the debt collectors know these lawyers are not familiar with the debt collection business and take advantage of them.

Pro se defendants who get YourLegalLegUp materials know what the lawyers who specialize know, but they are inexperienced in the courtroom and have to get used to the way courts work.

The lawyers for the debt collectors do not know what the pro se defendants know (at first) and (at first) do not expect or believe that the pro se defendants will continue to fight. As they do continue to fight, however, the pro se defendants become more experienced and comfortable in the courtroom, and the debt collectors become more aware of what the defendants know. They become willing to settle on much better terms because they can see that continuing to litigate will lose them money. As far as I can tell, the longer the pro se defendant is willing to keep fighting, the better the terms get, and often the debt collectors drop the case because they do not want to lose money.

We can help either way. Click on the Articles button on the menu bar above to go to publically available videos and articles,

© 2025 Your Legal Leg Up, All rights reserved